Bringing Flow to the Battery World (II)

This is the commercial part of the redox flow battery (RFB) technology overview. See the first part (technical overview) here. This article covers value proposition, market readiness, deployment history and scale up barriers of RFB systems.

Value proposition

RFBs typically serve applications similar to those served by lithium-ion batteries (LIBs). The applications include energy shifting, backup power, microgrids and ancillary services. However, the inherent features that make RFBs more attractive for the same applications are:

- Unlimited cycling: LIBs are typically constrained to 1 cycle per day to optimize capacity retention performance. RFBs can support multiple cycles per day without adverse impacts on capacity retention.

- Longer lifetime: unlike LIBs which typically offer a 10-year lifetime, RFBs can operate at the rated capacity for more than 20 years.

- Depth of discharge (DoD): unlike LIBs which are usually partially discharged to reduce capacity degradation, RFBs can achieve 100% DoD without loss in capacity retention.

- Lower safety risk: thermal runaways are the biggest safety threat in LIBs. RFBs are inherently devoid of fire risks due the absence of thermal runaway. The bulk electrolytes in RFBs act as cooling reservoirs due to their high thermal mass. Thermal mass refers to the rise in temperature per amount of heat absorbed.

- Lower marginal cost of storage: marginal cost refers to the cost of an extra kWh worth of energy storage capacity. The decoupling of energy and power in RFBs makes increasing the energy capacity of an RFB theoretically cheaper than the same in a LIB.

Market readiness

The technology readiness level (TRL) and commercial readiness index (CRI) of redox flow battery technologies vary by chemistry. The most developed flow battery chemistry is the vanadium redox flow battery (VRFB). VRFB has a TRL rating of 9 which means the technology has been fully tested and demonstrated at system level. From a CRI perspective, the VRFB technology has a rating of 4 which indicates multiple commercial deployments. Additionally, the CRI rating of VRFB reflects its current dependence on government support to scale up.

The TRL ratings of the rest of the RFB chemistries range between 5 and 9 while their CRI ratings are lower than 3.

Compared to LIBs, RFBs demonstrate lower roundtrip efficiencies, lower energy density and higher upfront cost. These factors have impeded the deployment of RFBs.

"The total installed capacity of RFBs is approximately 1000 MWh."

Major manufacturers and deployments

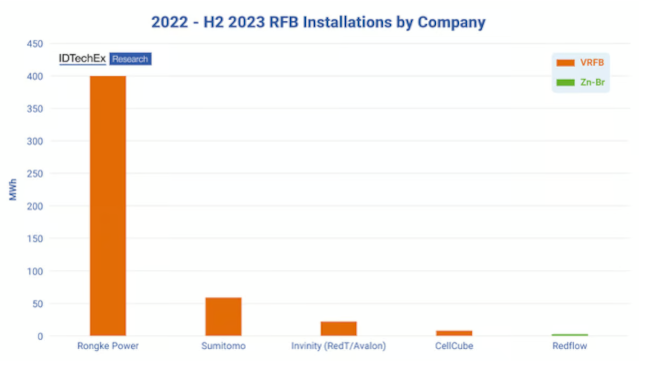

RFB Deployments by the major OEMs

The leading original equipment manufacturers (OEMs) of the RFB energy storage systems are Rongke Power, Sumitomo, Invinity, CellCube, Redflow and ESS. The total installed capacity of RFBs is approximately 1000 MWh. In comparison, the deployment of LIBs had reached 2,800,000 MWh by May 2023.

Rongke Power deployed the largest VRFB system to date, a 100 MW / 400 MWh system in Dalian, China. There are plans to increase the capacity of this plant to 800 MWh.

Sumitomo Electric is a Japanese company that has been deploying VRFBs since 2001. Sumitomo installed more than 50 MWh across the world between 2022 and 2023. The largest Sumitomo VRFB is a 15 MW/60 MWh installation in Hokkaido. The installation has been under commercial operation since 2019.

Invinity Energy Systems is an Anglo-American company with deployments across continents. Invinity has installed a total of about 25 MWh in the past year. Overall, Invinity has deployed or contracted over 75 MWh across 70 projects in 14 countries.

CellCube Inc., is an Austrian VRFB manufacturer with installations across several countries. CellCube has deployed a total capacity of 13.95 MW/75.29 MWh. In the year between 2022 and 2023, CellCube installed approximately 10 MWh.

VRB Energy is a VRFB OEM headquartered in Canada. VRB has deployed 45 MWh worth of capacity and is currently developing an additional 750 MWh.

The leading manufacturer of zinc-bromine RFB (ZBRFB) is Redflow. Redflow was founded in 2005 and is headquartered in Australia. Between 2022 and 2023, Redflow deployed close to 5 MWh. The largest ZBRFB installation to date has a 2 MWh rating.

The leading manufacturer of the all-iron redox flow battery is ESS Inc. ESS is in the process of deploying commercial systems but has several ongoing demonstrations.

DOE efforts

The US Department of Energy (DOE) has been running the Energy Storage Grand Challenge Storage Innovations 2030 (SI 2030) to support the commercialization of various alternative energy storage technologies including RFBs. SI 2030 has a levelized cost of storage (LCOS) target of USD 0.05/kWh for RFBs. LCOS is the quotient of the sum of the capital and the operating expenses of an energy storage system and its throughput over its useful lifetime. SI 2030 identified several challenges to the commercialization of RFBs which translate to cost reduction opportunities. The technological areas of improvement include membranes (higher selectivity and durability), electrodes (higher power density), development of low voltage power electronics, bipolar plates (more durable and cheaper) and electrolytes (domestic supply chains and cheaper). Non-technological areas of improvement include manufacturing processes, raw materials supply chains, demonstration projects and end of life management.

Conclusion

Investment in local raw material supply chains, better manufacturing processes and demonstration projects will help lower the risk profile of the RFB technology hence mass deployment.

3/21/2024 2:00:00 PM