Explore how and where marine aquaculture production will develop and meet growing demand through to 2050

Marine aquaculture is set to play a critical role in securing supplies of food for a global population that will exceed nine billion by 2050.

For the industry to grow sustainably, operators, governments and investors need trusted information on which to base business cases, supportive policies, and financial and technical due diligence.

This first Marine Aquaculture Forecast from DNV responds to that need by delivering our ‘best estimate’ of the future.

Our analysis considers population growth and changes in living standards to estimate future demand for food. We also consider growing concerns about health and sustainability, which will impact food preferences. It then forecasts the role of marine aquaculture in meeting this demand through the main species and technology options involved.

The forecast supports our view that future demand for seafood can only be met sustainably with a wave of technological innovation in marine aquaculture. Reaching these production levels requires innovation on many fronts, including technologies to intensify production.

How will demand for marine aquaculture develop, and how will this demand be met? See the highlights and download DNV's Marine Aquaculture Forecast to 2050.

0:34

1. Farmed seafood increasing its contribution to world food supply

Graph: Global marine aquaculture production approaches same level as capture fisheries by mid-century.

People will on average eat 10% more protein in 2050: With near 25% population increase by mid-century, protein consumption will rise more than 35%. Marine aquaculture will be vital to secure supplies of protein.

Marine aquaculture will more than double by 2050: As seafood demand rises with living standards and population growth, we forecast marine aquaculture production, excluding seaweed, will rise from 30 million tonnes per year (Mt/yr) live weight to 74 Mt/yr.

Marine aquaculture will approach the current output of marine capture fisheries. The output of capture fisheries is set to remain stable from now to mid-century as it has already reached its sustainability limits.

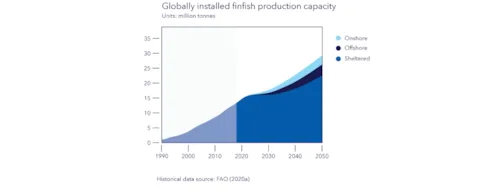

2. Innovation is needed to meet demand sustainably

Graph: Globally installed finfish production capacity.

Production onshore and further offshore will gain traction and market share. High-value finfish will increasingly be farmed in closed systems on land, and in larger production units in more exposed offshore locations. We predict 13% of farmed marine finfish production capacity being offshore in 2050, and 10% onshore.

Lower costs due to accumulated experience will drive technology uptake. Initial investments will be incentivized by favourable licensing schemes as new technologies address concerns such as fish health, pressure on inshore marine space, and environmental impacts.

New offshore technologies for finfish can increase yield and reduce space requirements: The total area is reduced by half in 2050 compared to if all production remained sheltered. By scaling offshore production of finfish, the average finfish food production per km2 can increase by around 10% to 850 tonnes per km2.

Transparency and traceability remain key to growth: Our findings underline how policies, mechanisms, and technologies encouraging and enabling transparency and traceability throughout the value chain are needed to accelerate sustainable growth of marine aquaculture production.

3. Contribution to food supply

Graph: Marine aquaculture production by species in 2050.

Farmed finfish is the most important contributor to world food supply from marine aquaculture. It has the most favourable live-to-edible weight ratio and the highest protein content. With new production technologies, and lowering costs, we believe that future focus will be on these high value species. Molluscs will remain the most farmed species by live weight.

Growth in industrialized seaweed production hinges on technology. There is growing interest in seaweed production in developed, high-cost countries where new technologies that reduce manual labour costs will be needed for the industry’s development.

4. Regional trends

Graph: Regional production in live weight in 2050.

Large regional differences in output will persist. For example, the great majority of marine aquaculture production will be in Asia, beyond which Europe and Latin America remain the major players.

Selected other regional forecast include: South East Asia sees continued growth of finfish marine aquaculture in sheltered waters; offshore fish farming gains a strong foothold in Greater China, Europe, and Latin America; and, onshore farming of marine species comes to fruition in Greater China, Europe, and North America.

Dive deeper: download the full Marine Aquaculture Forecast