UK and Ireland windiness 2022

Lower than long-term averages – what are the implications for you?

Monitoring and recording wind speed trends can provide valuable insights for assessing project performance. But interpreting, understanding, and acting on those trends is where the real value lies. So, what do the 2022 UK and Ireland wind results mean to you?

2022 wind speed trends

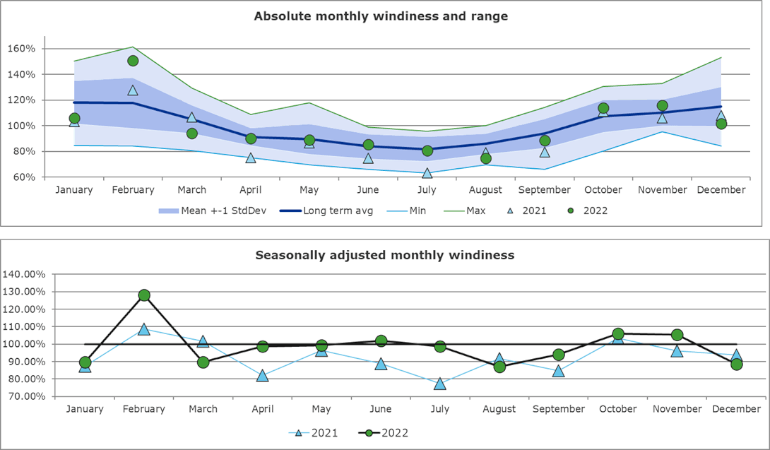

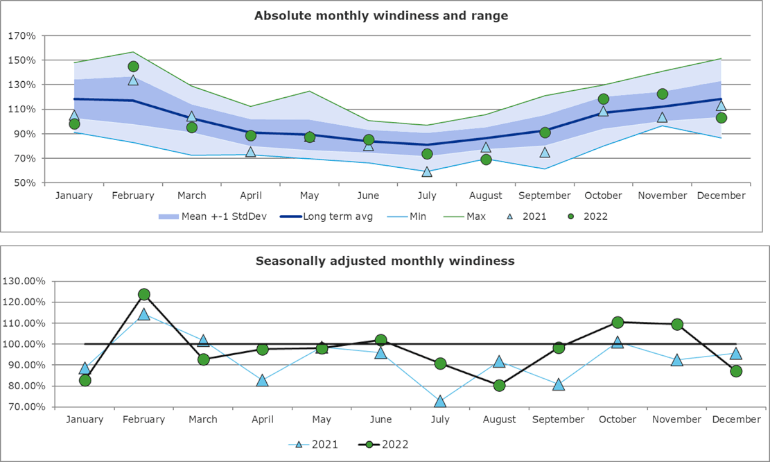

The windiness index followed a rather normal trend across 2022 based on the seasonality of wind resource in the UK and Ireland, except for in the month of February when winds were 28.3% higher than the long-term average in the UK and 23.7% in Ireland. The amplitude of the wind speeds which were consistently below average in 2021 were much closer to long-term averages in 2022. Most months would be considered normal and fall within the standard deviation of the long-term period. However, in the UK, March (89.6%) and August (87.0%) experienced wind speeds outside of the standard deviation and in Ireland, August (80.5%) saw the lowest wind speeds since 1996.

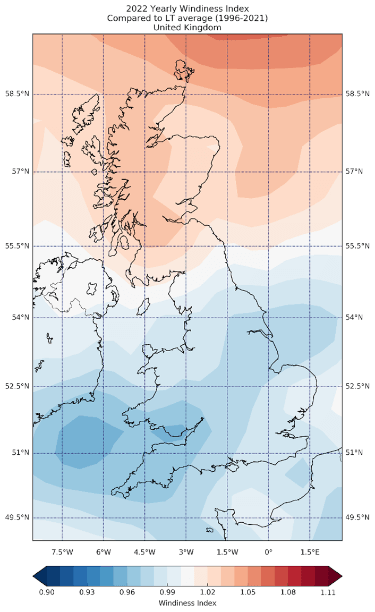

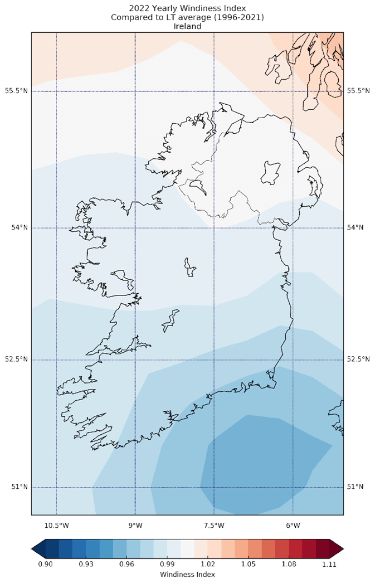

Overall, DNV’s UK Wind Index demonstrates that 2022 was approximately 1% less windy on average (coming in at 98.9%) than the 1996-2021 long-term reference, while the equivalent Irish results were very similar, being approximately 2% less windy (97.9%). A full breakdown of the monthly and quarterly wind indices for 2022 is given in the tables below, along with the ‘windiness’ for each complete year in the index. For ease of referencing, the monthly index for 2021 is also shown.

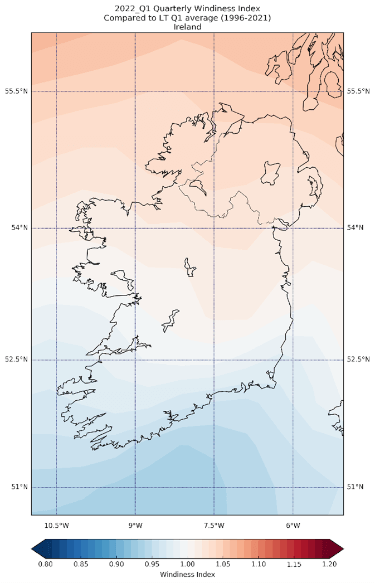

The year started slowly with January exhibiting wind speeds 10.3% and 17.2% lower than the long-term speeds in the UK and Ireland respectively, which is similar to what was experienced in 2021. Wind speeds in February were higher than average, in both the UK and Ireland and were outside of the standard deviation, +28.3% and +23.7% respectively. This is largely due to much stronger than normal wind speeds associated with Storm Eunice and also as a result of the less severe Storm Franklin which occurred within a week of each other in February. March wind speeds were lower than usual (-10.4% in the UK and -7.3% in Ireland). In the UK, the first three months of the year were 2.0% higher than the respective mean mainly due to the storms of February (128.3%) but in Ireland conversely, the same period was 1.0% lower than the respective mean due to the weak wind speeds in January and March (82.8% and 92.7% respectively).

Wind speeds for April, May and June were very similar to the long-term average in both the UK and Ireland (98.6%, 99.3% and 101.9% for the UK and 97.7%, 98.0% and 101.9% for Ireland). The index for April, May and June was calculated at 99.9% for the UK and 99.1% for Ireland, highlighting the similarity to the long-term mean.

In the UK, July and September experienced slightly weaker wind speeds than usual (98.8% and 94.1% respectively) although very close to the long-term average. August wind speeds in the UK were lower than average (87.0%), and outside of the standard deviation. Similarly in Ireland there were lower than usual wind speeds in July, August and September with a windiness index 89.9% for this three-month period. Ireland experienced its lightest August wind speeds since 1996, 19.5% less than the long-term average. Wind speeds were close to the long-term average in Ireland in September (98.4%).

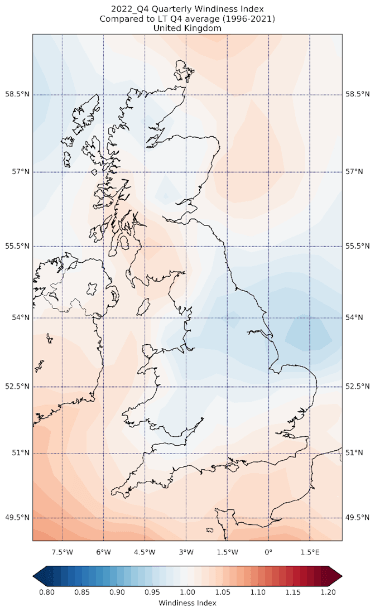

Wind resource became slightly stronger than normal levels in October and November (UK +6.1% and +5.4% respectively, Ireland +10.4% and 9.5% respectively). However, in December wind resource dipped below the normal (UK -11.6%, Ireland -12.9%) and as a result the seasonal quarterly index was slightly lower than normal in the UK (99.7%). The higher-than-normal wind speeds in October and November offset the lower wind speeds in December and the resulting seasonal index was 101.9% in Ireland.

Regional variations

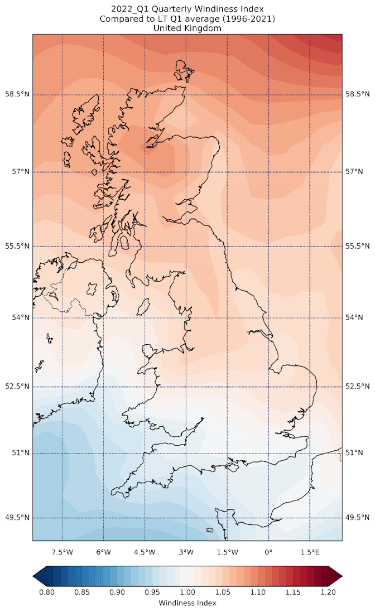

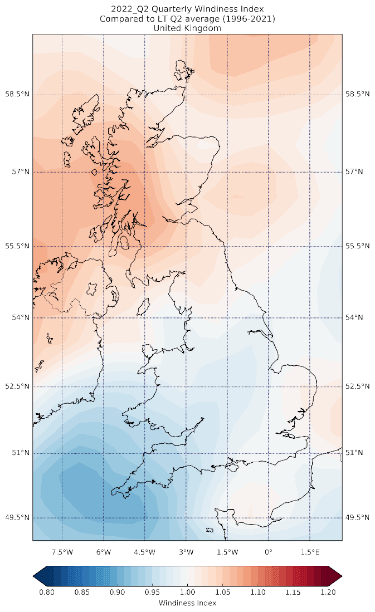

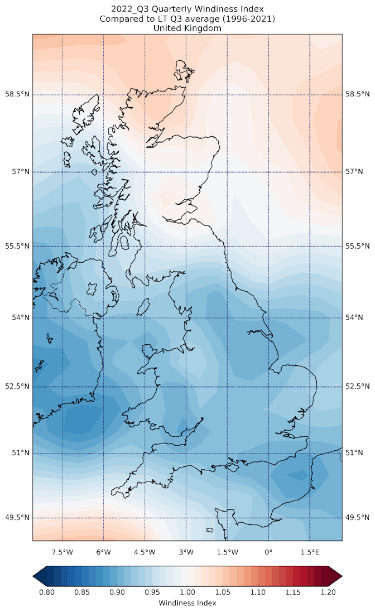

It is also important to consider the spatial distribution of the wind regime across the countries during the last year. Looking at the windiness maps for the UK below, we can observe that despite the entire country observing negative trends for the year, wind farms in the north of England, Scotland and Northern Ireland had slightly higher wind speeds than usual in the first six months of the year. However, in the second six months of the year lower wind speeds were observed throughout the UK except for small parts of Scotland.

|

|

|

|

|

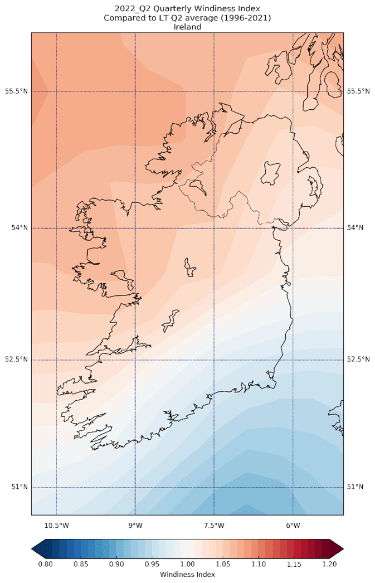

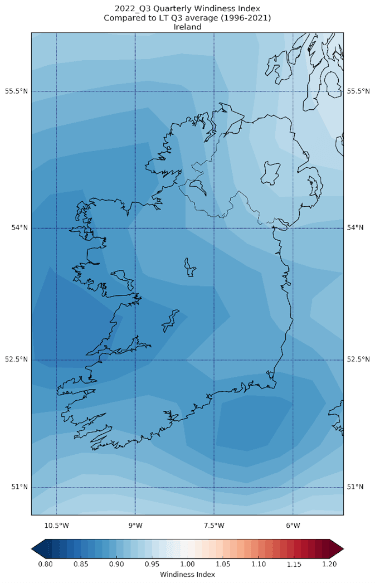

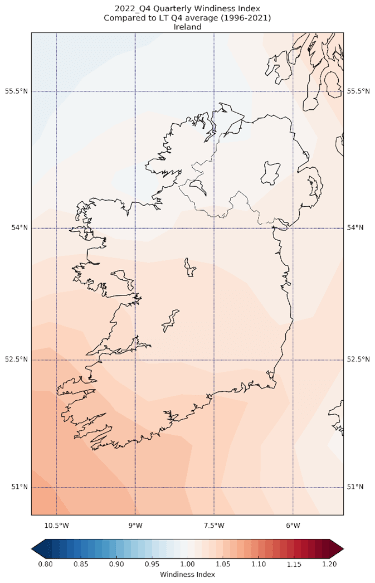

In Ireland, it can be observed that in the first six months of the year, the south of the country experienced negative trends while areas north of the midlands saw slightly stronger wind speeds. In the third quarter the entire country saw negative trends. Wind farms in the southeast of Ireland observed larger negative deviations as a negative anomaly centre could be observed at the Irish Sea and along the Atlantic coast. Only in the fourth quarter did the southeast of Ireland experience positive trends in wind speeds.

|

|

|

|

|

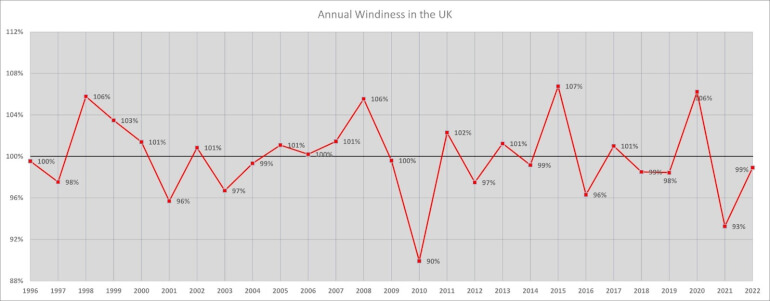

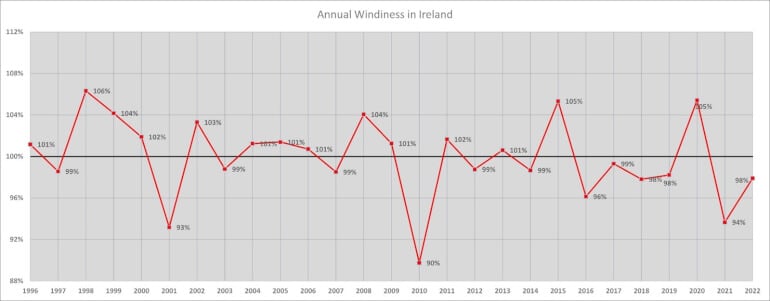

Long-term averages

For clarity, long term graphs for both the UK and Ireland are shown to illustrate the fluctuation of windiness indices since 1996.

Interpreting the data to establish an answer

Annual windiness remained lower than average in 2022, although it has recovered from the significant drop in mean wind speeds from 2021 (+4% from 2021 to 2022). What does this windiness index mean for wind farm owners, investors, and developers? All other things being equal, wind farm owners can expect to have seen lower production at UK and Irish projects during 2022, compared to the long-term, because of the decreased windiness. Using typical project wind speed to energy sensitivity ratios, it is noted that a 2% drop in wind speed corresponds to a decrease of approximately 3-4% in terms of energy production. This should be taken into consideration during reviews of project performance. Investors will have seen higher energy productions in their wind projects when compared to 2021. This is mainly due to higher wind resources in February and wind resources closer to the long-term average in Q2 and Q3.

Wind farm developers who have been conducting wind measurements during 2022 can also expect the average wind speed to be lower than the long-term average but higher than the same period in 2021. This trend should be taken into consideration when adjusting measurements to be representative of a long-term period.

The UK and Irish Wind Indices

DNV maintains a UK and Ireland Wind Index, which enables owners and investors to assess the performance of potential or operating projects. Likewise, the Wind Index is a robust tool for wind farm developers, empowering them to understand the ‘windiness’ of their wind monitoring campaigns compared to a long-term period.

The long-term reference period represents all years between 1996 and the year prior to the analysis. The UK and Irish Wind Index is normalized so that the average wind speed over the long-term period is 100%. The windiness of any given period is expressed as a percentage of the long-term average wind speed. Thus, a value exceeding 100% indicates that a period was windier than the long-term average, whilst a value below 100% suggests that a period was less windy.

Seasonal effects

Wind speeds in the UK and Ireland exhibit strong seasonality, with a tendency for higher wind speeds during the winter months and lower wind speeds during the summer months. As a result, DNV also derives a seasonally adjusted Wind Index, which has been corrected for seasonal bias.

To be more precise, the windiness of any given period is expressed as a percentage of the long-term average wind speed for that specific period. For example, the long-term windiness of the month of January is 118%. If a specific (individual) January has an index value of 123%, the seasonally adjusted value for that January would be 123%/118% = 104% (+4%).

About DNV

DNV offers a new service for generating bespoke monthly Windiness Reports for your portfolio. This includes an average of your entire portfolio and a breakdown of each one of your assets. For more information, please contact Doireann Kavanagh. Learn more about our full range of services and products.

2/27/2023 8:00:00 AM