2023 was a pivotal year for HVDC. What can we expect next?

An overview of the major trends and developments to date and what we can expect in 2024.

Last year was nothing short of transformational for HVDC technology and will shape the industry for the next decade. We saw unprecedented levels of investments and contract awards, creating a firm project pipeline and enabling the industry to make the required investments in the supply chain to increase much-needed production capacity. Even though most activity took place in Europe [1], 2023 was also the year in which the U.S. got serious about its HVDC renaissance, with major government support packages awarded and several HVDC projects breaking ground. Providing a glimpse into the future, several hybrid or multi-purpose infrastructure projects were announced, combining both offshore wind export and interconnection functionality, requiring multi-terminal HVDC technology. A few European grid operators also presented long term strategic grid plans including key roles for multi-terminal HVDC overlay grids as the bulk electrical energy carrier of choice.

New commissioned capacity and technology leaps

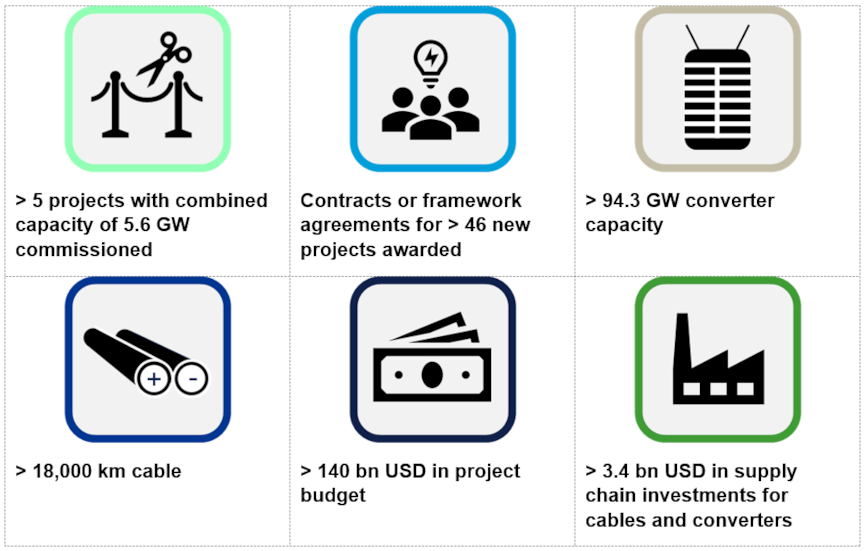

Five new HVDC projects reached completion and were commissioned, bringing another 5.6 GW of combined HVDC transmission capacity online--significant but modest increase, given the scale at which transmission capacity needs to be build out. It included the 1400 MW 765 km Viking Link the world’s longest interconnector. A few technology leaps were made, such as the commissioning of Dogger Bank A, the first application of lean and unmanned offshore HVDC station concepts as well as the first to use a 66 kV direct connection, driving down costs of offshore HVDC further. It also included the first application of Controllable Line-Commutated Converter (CLCC) technology to a HVDC transmission link in China, realizing a reliable recovery process and controllable commutation through combining fully controllable IGBT devices and semi-controllable thyristors. The resulting converter is immune to commutation failure yet benefits from the cost effective and robust characteristics of thyristor based converter technology[2].

Gigantic contract and framework agreement awards

The big take away from 2023 is the sheer volume of tenders and frameworks that were announced and/or awarded throughout the year. Worldwide, this included at least 46 new HVDC projects to be installed over the next decade, equating to a 94.3 GW addition of HVDC transmission capacity, and at least 18.000 km of HVDC cable. All converter tenders assumed the use of VSC technology. The vast majority of these are 525 kV, 1.8-2 GW bipole projects. The publicly announced investment is 140 bn USD, which will be significantly higher if one adds the non-disclosed budgets. This huge investment is driven predominantly by two European transmission system operators, starting with the Dutch-German 30 bn EUR TenneT framework agreement, which at the end of the year was dwarfed by the British 59 bn GBP National Grid tender. These behemoth tenders overshadowed what would otherwise be groundbreaking contract awards such as the 3x3 GW NEOM HVDC project in Saudi Arabia. Notably, in 2023, Mitsubishi won a contract to build a 300 MW back-back converter station in Japan, a first time HVDC application of its Diamond VSC technology, setting the scene for new players to enter the converter supply chain which has traditionally been dominated by three European manufacturers.

Supply chain investments

The announcement of the mega tenders has sent shockwaves through the supply chain and has increased the delivery times for offshore HVDC systems to well within the 2030’s if ordered today, jeopardizing offshore wind deployment targets across the world. To fulfil this huge order book and speed up production, OEMs have been making investments in cable and converter manufacturing capabilities. At least 3.3 bn USD is being invested in new HVDC cable factories and capacity expansions worldwide. Similarly, investments are being made in HVDC valve manufacturing capacity through new factories, expansion of existing facilities and industry collaborations. However, all new manufacturing capacity is based in Europe, Middle East and in Asia, not yet in the U.S.

Similarly, investments were announced in the other critically important industry of installation vessels. New cable laying vessels were commissioned or ordered by Van Oord, Jan de Nul, Prysmian, Nexans and NKT.

The U.S. is back in HVDC town

After pioneering many aspects of HVDC technology, the U.S. experienced a slowdown in new-built HVDC transmission capacity in recent decades, often due to regulatory, permitting and policy hurdles as well as financing challenges. Many system operators and regulatory bodies are seen as taking a conservative approach towards HVDC technology and fail to consider the capabilities, characteristics, and maturity of today’s state-of-the-art. But 2023 saw a hive of activity, including calls for FERC to hold a technical conference on HVDC capabilities, HVDC workshops at MISO and ERCOT, and the publication of an industry-sponsored report on the operational benefits of HVDC technology, and the award of two HVDC projects in CAISO under a FERC 1000 competitive transmission solicitation process.

Most notably, several concrete steps towards realization of, in some cases, decade-old HVDC plans were made. First of all, a large number of HVDC transmission projects such as the Transwest Express (TWE), Grain Belt Express, SOO Green, the NECEC project received critical permitting and regulatory approvals, clearing the way for construction to start (or resume in the case of NECEC). Several projects such as TWE, Champlain Hudson Power Express (CHPE), and the Sunrise offshore wind farm connection did not waste time and broke ground last year.

As a reminder of some of the hurdles that HVDC projects continue to face, Pecos West was denied a certificate of convenience and necessity, shining light on the continuing barrier of the right of first refusal rules to competitive HVC transmission building.

From a financing perspective, recognizing a chicken-and-egg situation in capacity offtake agreements between renewable generators and transmission developers, the Department of Energy (DOE) awarded its first ever anchor tenant contracts, including Twin States Clean Energy Link, aimed at enabling transmission developers to get the financing to start construction[3]. Minnesota Power received a 50 million USD DOE grant to upgrade the Square Butte HVDC line. Separately, for its Sunzia project, Pattern Energy closed the largest clean energy infrastructure project in U.S. history for $11 billion financing. EnergyRe announced its capital raise of $1.2 billion to support its HVDC developments such as CPNY, SOO Green, and Leading Light offshore wind farm, including a stake by WindGrid which is subsidiary of the Elia group which also owns the Belgian and German grid operators Elia TSO and 50Hertz, respectively, and brings in significant HVDC expertise.

Two new offshore transmission solicitations were announced: the Public Policy Transmission Need (PPTN) in New York, and the State Agreement Approach 2.0 (SAA) in New Jersey. Both solicitations will be building on experiences from previous rounds and are very likely to require the use of offshore HVDC technology to minimize the impact on environment and local communities. In preparation for the New Jersey PPTN, Invenergy announced its acquisition of Blackstone’s Atlantic Power Link portfolio which was developed for the previous SAA 1.0, renaming it Jersey Link.

Formerly, limits on maximum circuit capacity due to the most severe single contingency limits meant that submitted solutions did not include HVDC technologies’ state-of-the-art of 2 GW, 525 kV solutions. Acknowledging that such solutions hold societal benefit, ISO-NE requested NYISO and PJM to jointly study solutions that would enable 2 GW bipole links through the Joint ISO/RTO Planning Committee (JIPC).

Actively driving developments in technology and standardization, the DOE announced its $8.5 million WETO FOA awards to 4 projects addressing barriers to the realization of High-Voltage Direct Current for Offshore Wind Transmission. DNV, as one of the awardees, formed a consortium of 10 offshore wind and transmission developers to identify barriers to the use of High Voltage Direct Current transmission in the U.S. grid in a Joint Industry Project (JIP).

Rise of hybrid projects

Hybrid interconnectors or multi-purpose infrastructure are the first stepping stones towards true multi-terminal HVDC grids. They realize cost savings and operational benefits by combining the functions of offshore wind export with that or interconnecting different markets and/or reinforcing the onshore AC grid by means of an offshore connection. An early version of such a link was realized by the Kriegers Flak ‘Combined Grid Solution’, connecting two offshore wind farms whilst realizing trading capacity between Denmark and Germany. The Kriegers Flak project uses high voltage AC cables and an onshore back-to-back HVDC converter, as Germany and parts of Denmark are in different synchronous zones. The next generation of multi-purpose grids are likely to be based on HVDC and drive the uptake of multi-terminal technology. Because these first multi-purpose systems typically require a limited number (3 or 4) of converters, they can can still be reasonably competitively procured from a single vendor, avoiding any multi-vendor interoperability issues. Moreover, because the projects are often small enough to not need an HVDC circuit breaker, they avoid the associated technology maturity and limited supply chain issues.

Previously announced projects such as the Nautilus Link between the U.K. and Belgium are steadily progressing. A whole slew of announcements regarding multi-purpose interconnectors were made in 2023. The U.K. and Netherlands unveiled plans for the multi-purpose interconnector LionLink. Estonia and Germany signed a letter of intent to develop a new hybrid interconnector Baltic WindConnector project. Similarly, Denmark and Germany signed a memorandum of understanding to ‘explore perspectives’ on developing a potential hybrid interconnector between the two countries. And more concretely, the German and Norwegian grid operators Amprion and Statnett agreed to jointly investigate the feasibility of a hybrid interconnector.

Unstoppable momentum towards multi-terminal multi-vendor systems

Several multi-terminal HVDC developments are currently underway in Europe. Progress towards Europe’s first VSC multi-terminal system, the Scottish Caithness-Moray-Shetland extension, is in its final phase with the start of cable laying, and on track to be commissioned in 2024. In the meantime, preparations are being made for tendering the multi-terminal HVDC equipment needed to connect the Bornholm island to the Danish and German mainland. As an industry first, the tender tellingly includes requirements for the optional extension of the system with HVDC circuit breakers. Similarly, in Germany, the four grid operators TenneT, Amprion, 50Hertz and TransnetBW are jointly developing three multi-terminal HVDC hubs to connect HVDC offshore wind export links directly with onshore HVDC links to bring the wind power down south, avoiding the investment in additional converters and the operational energy losses in such converters. Similarly, in the U.K., the Aquila project, run jointly by SSE and National Grid and aimed at delivering the first demonstration of multi-vendor operation of a VSC-HVDC network outside of China, is gathering steam.

To drive technology and standardization towards such multi-terminal and multi-vendor system integration, the European Union funded two research, development, and demonstration projects. The Ready4DC project wrapped up in 2023, providing a legal framework for the multi-vendor cooperation and a basis for the subsequent InterOpera project, which aims to solve the technical coordination needed to ensure multi-vendor cooperation.

Anticipating a future in which HVDC circuit breakers will play a critical role in safeguarding reliability, the supply chain is making preparations. Thus far, only Hitachi can deliver both converters and an HVDC circuit breaker, limiting the supply chain and the ability for grid planners to competitively procure HVDC circuit breakers. However, Mitsubishi acquired Scibreak, a Swedish start-up, enabling Mitsubishi’s high voltage manufacturing capabilities to be combined with the Scibreak HVDC circuit breaker concept. In a next move, Mitsubishi also teamed up with Siemens to jointly develop HVDC switching station concepts including the Scibreak breaker. GE teamed up with SuperGrid institute to jointly develop the latter’s HVDC circuit breaker concept, hopefully soon adding a third vendor to the mix.

A glimpse of an HVDC overlay grids based future

Providing a view of the future, two major grid operators in Europe announced their long-term transmission plans, which both rely heavily on both an offshore and onshore HVDC overlay grid for bulk power transmission. The Italian grid operator Terna introduced the HyperGrid, their vision of a future Italian power grid in which HVDC connections reinforce the onshore AC grid by running underwater along the Italian coast, as well as submarine connections to the Italian islands. In the Netherlands and Germany, the grid operator TenneT, which previously launched the 2 GW program, presented their vision for an integrated future energy system called Target Grid. This futuristic grid concept, which assumes deep electrification, features high-power networked HVDC ‘super-highways’ connecting offshore resources with onshore load centres deep inland, and providing offshore paths for bulk power flows to avoid overloading the AC grid. Both the HyperGrid and Target Grid visions may seem to be futuristic, but they provide a clear signal that HVDC technology has become a trusted tool in the grid planner’s toolbox.

References:

[1] Asian developments have not been considered in these numbers even though large plans are in place in China and India, but not as much information is publicly available

[2] https://news.xinmin.cn/2023/06/20/32408901.html

[3] Unfortunately, in disappointing news in 2024, National Grid decided to pull out of the Twin States Clean Energy Link. A sign that a lot still needs to be done on improving the cross-border U.S.-Canada power market integration.

3/15/2024 2:00:00 PM