What is the UK ETS?

The UK Emissions Trading Scheme (UK ETS) is the United Kingdom’s cap‑and‑trade mechanism for reducing greenhouse gas emissions. From 1 July 2026, the scheme will apply to the maritime sector, covering cargo and passenger vessels of 5,000 GT and above. Offshore vessels of the same size threshold will be included from 1 January 2027.

The implementation timeline for shipping

The UK ETS is being phased into maritime transport, entering the scheme on 1 July 2026, with the first scheme year covering the period from 1 July to 31 December 2026. Offshore vessels are being brought into scope from 1 January 2027. Surrender obligations for the first shipping scheme year will take place in 2028.

According to The Merchant Shipping (Monitoring, Reporting and Verification of Carbon Dioxide Emissions) (Revocation) Regulations 2026, UK MRV requirements were revoked with effect from 3 April 2026. From 1 July 2026, maritime emissions fall under the UK ETS.

The scope of the UK ETS directive

For maritime transport, the UK ETS applies to emissions generated during domestic UK voyages, including voyages that start and end at the same UK port. Emissions produced during port stays at UK ports are also included, even when linked to international voyages. In addition, emissions generated during ports of call are within scope, including time spent at berth, whether moored or anchored, at UK ports and offshore installations.

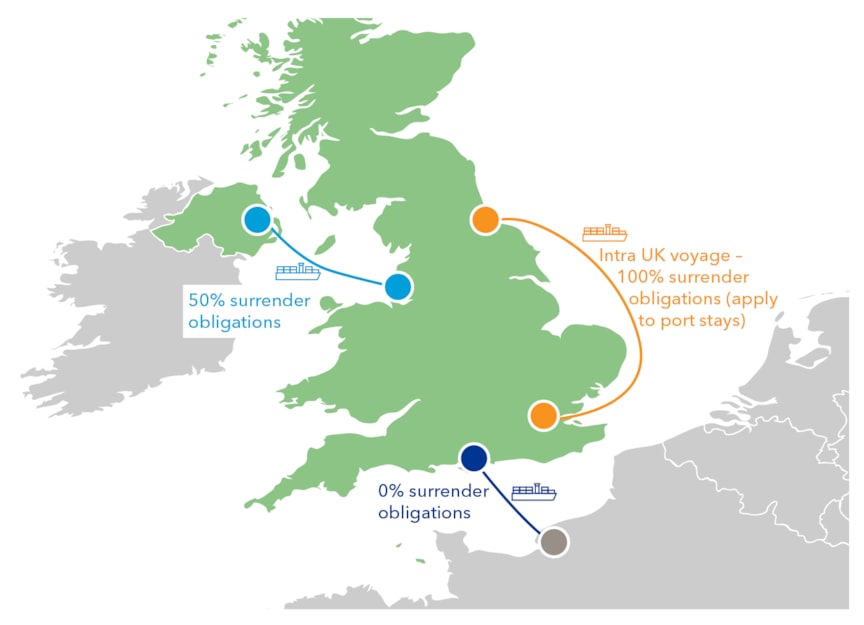

The following figure illustrates the principles for a voyage between Northern Ireland and Great Britain, where the surrender obligation, is 50%, while port stays in both Northern Ireland and Great Britain are subject to a 100% surrender obligation. For a voyage between France and Great Britain, there is no (0%) surrender obligation for the voyage itself; however, the port stay in Great Britain remains subject to a 100% surrender obligation.

The scheme covers carbon dioxide (CO₂) as well as methane (CH₄) and nitrous oxide (N₂O) emitted on a tank‑to‑wake basis. CH₄ and N₂O are reported as CO₂‑ equivalent emissions using IPCC AR5 global warming potential values. Carbon dioxide emissions from biofuels are treated as zero.

Certain activities and vessel types are excluded. These include government non‑commercial vessels, fishing and fish‑processing ships, and vessels operating a Scottish ferry service.

Voyages between the UK and non‑EEA ports, as well as UK Overseas Territories or Crown Dependencies, are not considered domestic voyages. For voyages between Northern Ireland and Great Britain, a 50% reduction in surrender obligation applies.

UK ETS cost implications for shipping

Shipping companies must purchase and surrender UK allowances (UKAs) corresponding to their verified emissions that fall within the scope of the UK ETS. The number of allowances required is based on the annual verified emissions after the application of any relevant exemptions or reductions. UKA prices are determined by market conditions.

Responsibility for UK ETS compliance lies with the maritime operator, defined as the registered owner by default, unless responsibility is formally transferred to the ISM company through a legally binding agreement.

Related links

The UK ETS expands to maritime from 1 July 2026

Read our Technical and Regulatory News from 5 June 2026

MRV – Monitoring, Reporting and Verification (EU and UK)

Visit our topic page

EU ETS

Visit our topic page

FuelEU Maritime

Visit our topic page

UK Emissions Trading Scheme for maritime: how to comply

Find a comprehensive guidance published by the UK Environment Agency