FSRUs gaining strategic importance in a changing LNG landscape

Once deployed primarily in response to short-term supply disruptions, FSRUs are increasingly being repositioned as long-term infrastructure. As LNG markets expand and energy systems evolve, their role is being reshaped by the need for flexibility, faster deployment, and reduced investment risk.

The role of floating storage and regasification units (FSRUs) is shifting rapidly. Traditionally viewed as rapid-deployment tools, FSRUs have, in recent years, evolved into long-term strategic infrastructure, shaped by global market developments and the growing need for energy-source flexibility. This shift reflects structural changes in LNG trade flows, heightened energy security concerns, and increasingly stringent regulatory expectations.

FSRUs are emerging as one of the fastest and most flexible ways to add LNG import capacity.

Background: From global energy security to energy-transition facilitators

Following the escalation of the Russia–Ukraine conflict in 2022, and the resulting disruption of pipeline gas flows into Europe, FSRUs were rapidly deployed as critical tools to secure energy supply. Their ability to mobilize quickly, integrate into existing networks, and diversify import sources proved decisive during a fast-moving crisis. Since then, however, global interest in FSRUs has expanded well beyond emergency response, as countries reassess longer‑term import strategies and infrastructure needs.

As many markets plan for a prolonged energy transition, floating regasification infrastructure is increasingly seen as a pragmatic way to maintain access to natural gas while still investing in low‑carbon alternatives. FSRUs allow policymakers to avoid the cost and lock‑in associated with onshore terminals, while their deployment offshore also reduces land-use conflicts, planning complexity, and community impact.

LNG market expansion and the need for flexibility

The rising prominence of FSRUs also reflects the rapid expansion of the global LNG market.

Global export capacity is expected to grow by 35% by 2027, with around 230 million tonnes per annum (mtpa) of new liquefaction capacity coming online by the end of the decade. The United States is expected to add 108 mtpa of new capacity between 2025 and 2029, more than doubling its current export capability, while Qatar will add another 65 mtpa by 2030, bringing its total output to 142 mtpa. At the same time, ongoing geopolitical tensions in the Middle East, particularly around critical chokepoints like the Strait of Hormuz, underscore more than ever the need for flexible and resilient energy solutions.

These dynamics are especially challenging for emerging LNG‑importing economies, where exposure to price volatility can create economic, fiscal, and logistical pressures during periods of market stress. Countries such as Bangladesh and Pakistan have previously curtailed LNG imports during price spikes, highlighting the financial vulnerability associated with reliance on spot LNG. If price volatility persists, newly planned import infrastructure risks being underutilized, delayed, or in some cases cancelled altogether, strengthening the case for solutions that allow capacity and risk to be managed more flexibly.

FSRUs as a flexible and resilient import solution

Against this backdrop, FSRUs are emerging as one of the fastest and most flexible ways to add LNG import capacity. Unlike onshore terminals – where land availability, public opposition, planning approval, and construction timelines can delay projects for years – FSRUs can be deployed at relatively short notice once contracted.

As a result, most new LNG import terminals outside East Asia are opting for FSRUs. Since 2022, nearly all new European facilities have been ship-based FSRUs, with similar trends emerging in South Asia, Southeast Asia, and the Americas. China remains the exception, continuing to favour large onshore terminals as part of its long-term infrastructure strategy.

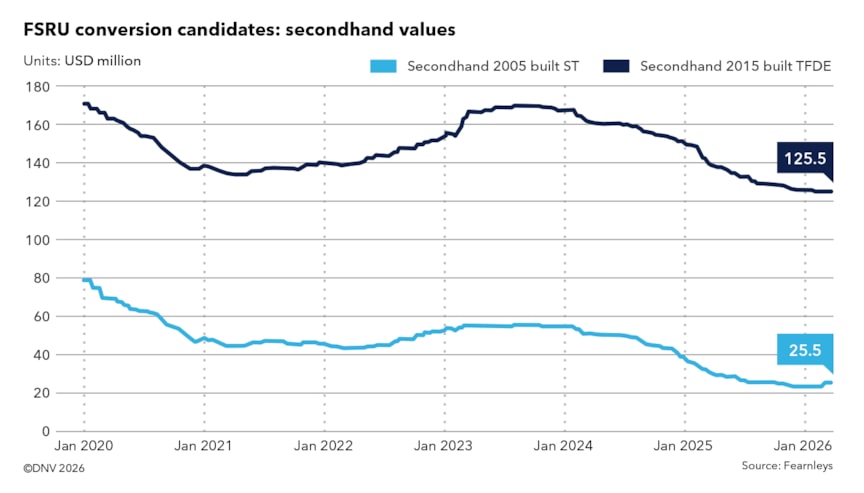

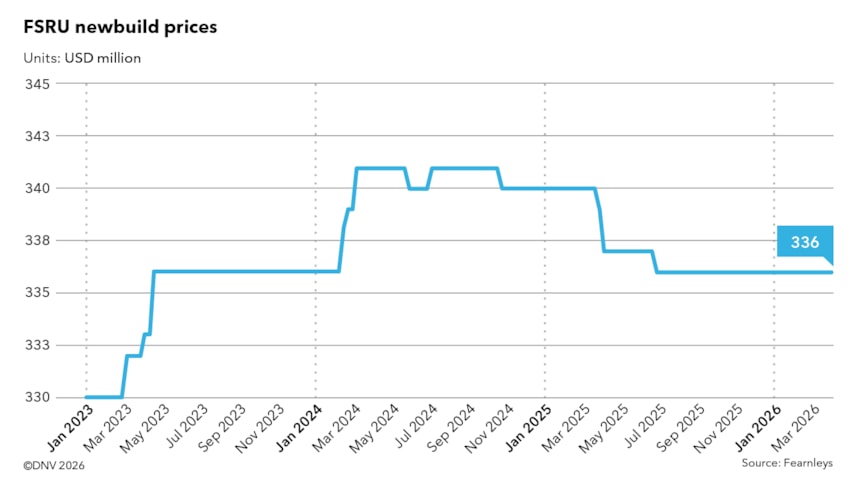

Conversions taking precedence over newbuilds

The expanding LNG supply picture is also shaping how new FSRU capacity is being added. LNG carrier conversions are expected to dominate fleet growth in the coming years, driven by a growing pool of older vessels that are becoming less competitive on traditional long-haul trades due to efficiency and size constraints. This is creating a steady pipeline of candidates suited for conversion to FSRUs or floating storage units (FSUs).

The commercial case underscores the appeal: conversion projects can typically be completed in roughly nine months of yard time and around two and a half years from final investment decision to full operation. This is significantly faster and generally less capital-intensive than commissioning a newbuild unit.

Newbuild FSRUs remain relevant, but mainly for charterers and regions seeking multi-decade commitments and the highest levels of reliability. In these cases, purpose-built vessels may be specified to meet long-term operational requirements.

However, for most projects, the speed to market and cost efficiency of conversions will ensure they remain the primary driver of fleet growth in the coming years.

A stable but highly specialized charter market

Despite rapid change across the wider LNG landscape, the FSRU charter market remains comparatively stable, albeit with measured growth in recent years. The global fleet numbers only around 50 units, and projects are typically structured around long-term, project-specific requirements. Unlike the LNG shipping market, where spot rates and short-term charters can fluctuate sharply, FSRU deployment is dominated by multi-year commitments that typically span five, ten, fifteen, or even twenty years.

This contractual structure largely insulates the segment from the volatility seen in LNG carrier markets. Charter rates are influenced far more by the project-specific factors, such as location, configuration, technical requirements, and contract duration, than by short‑term market swings. As a result, FSRU deployment continues to be shaped by bespoke national and industrial requirements rather than trading dynamics.

Power demand and energy efficiency in FSRU design

Environmental scrutiny is another increasingly influential factor in FSRU design and operation. Regasification is an energy-intensive process, requiring substantial onboard power to pressurize and vaporize LNG before delivering gas into national grids, power stations, bunker vessels, and, in some cases, road-based distribution networks. Typical regasification power demand can reach around 20 MW, making installed power capacity a key consideration when selecting conversion candidates or specifying new units.

Most FRSUs generate this power using their own LNG inventory, placing greater emphasis on fuel efficiency and emissions control. Vessel configuration also plays an important role: steam turbine LNG carriers typically require additional dedicated power-generation capacity when converted, while diesel electric vessels with multiple generator sets are generally better suited to handling regasification loads. Slow-speed two-stroke vessels often require supplementary equipment, despite having total installed power capacities typically around 25 MW.

Shore power integration is also becoming more relevant. However, its potential to reduce onboard fuel consumption and emissions depends heavily on grid availability, connection infrastructure, and the carbon intensity of the supplying grid.

Environmental and regulatory scrutiny of FSRU operations

Methane‑slip mitigation is another growing consideration for FSRUs. Operators are increasingly expected to adopt technologies and operating practices that reduce unburned methane emissions during regasification and auxiliary power generation, reflecting methane’s high global‑warming potential.

Beyond emissions, cooling‑water systems, specifically the choice between open‑loop and closed‑loop configurations, are facing increased scrutiny as regulators tighten expectations around seawater intake and discharge. Australia has led this trend, with other regions beginning to follow. Noise and vibration impacts on marine ecosystems are also receiving greater attention, reflecting a broader shift towards more locally focused environmental requirements within permitting and approval processes.

An LNG carrier transferring cargo to an FSRU moored at the Wilhelmshaven terminal in Germany.

Classification, operational flexibility, and long‑term performance

With environmental and technical expectations rising, the importance of robust classification support in the FSRU and FSU segment is greater than ever. Technical class notations developed specifically for these units play an important role in ensuring durability, operability, and compliance with evolving regulatory and operational standards.

Among these, DNV’s Alternative Survey Programme (ASP) and Under Water Inspection in Lieu of Drydock (UWILD) have become particularly relevant tools for both newbuild and conversion projects. Originally introduced to reduce downtime by extending internal cargo tank survey intervals while maintaining the same level of safety, these notations allow extended operations without drydocking and are now widely specified for FSRU and FSU projects, supporting higher operational availability, improved life cycle management, and more efficient station keeping. Having pioneered these approaches almost a decade ago, DNV now has more than ten units operating successfully under ASP and UWILD, in cooperation with multiple flag states.

For converted LNG carriers, in particular, classification and tailored notations play a critical role in enabling older hulls to meet modern safety, environmental, and operational expectations. As more units transition to long‑term stationary service, the ability to optimize operational uptime while maintaining safety and compliance is becoming a defining feature of successful deployment strategies.

Floating regasification infrastructure is a pragmatic way to maintain access to natural gas while still investing in low‑carbon alternatives.

Looking ahead: A more complex, but increasingly essential role

With global LNG supply continuing to grow and national energy systems becoming more diversified, the importance of FSRUs is expected to increase further. Demand is set to expand in regions such as South America, Southeast Asia, and Oceania, where rising energy needs, limited land availability, and long‑term decarbonization planning are driving interest in flexible LNG import solutions.

At the same time, future FSRU deployments will face a more complex operating environment. Environmental requirements will continue to tighten, cyber security considerations will grow as FSRUs become part of critical energy infrastructure, and expectations for reliability and availability will increase as markets become more dependent on floating import capacity.

Despite these challenges, the core strengths of FSRUs – speed, flexibility, and adaptability – will continue to position them as increasingly vital components of the global energy system. As countries continue to navigate a complex energy transition, FSRUs will remain a key enabler of secure, responsive, and cost‑efficient access to LNG.