How green molecules can create a more resilient income floor for agriculture

By Jan Willem Turkstra, Wouter van der Goot

This article completes our three-part series on green molecules strategy, using European case studies to demonstrate how biomethane, biogenic CO₂, and multipurpose crops act as strategic enablers of Europe’s energy and agricultural system.

Why green molecules matter for agricultural resilience

Agriculture has long been exposed to structural volatility. Prices swing with harvest outcomes, currency shifts, trade disputes, and increasingly with climate extremes. For farmers, this volatility translates into cycles of distress with occasional moments of relief[1]. When markets are oversupplied, products can be pushed below cost price[2]; when supply tightens, prices rise sharply, putting pressure on affordability and food security. The result is a system that is difficult to plan around and fragile for both farmers and society.

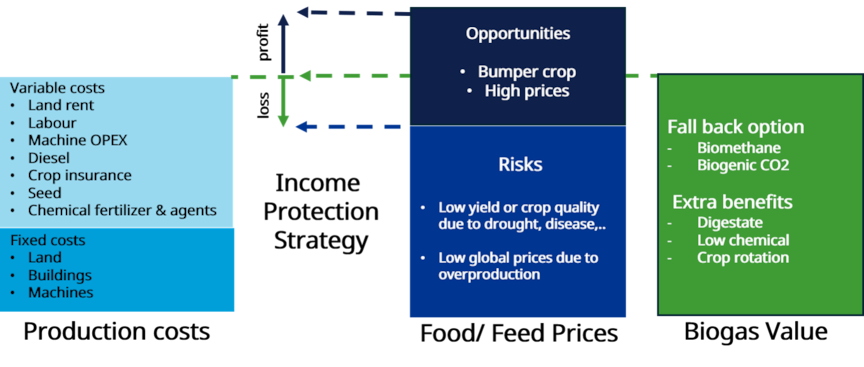

Yet agriculture still lacks a robust fallback mechanism when food and feed markets are saturated. This is where green molecules provide a more strategic role. Biomethane and biogenic CO₂ can create an alternative value stream for residues, manure, and surplus crops by turning them into storable, tradable energy products. Instead of being pushed into weak markets at marginal value, excess biomass can be redirected into biomethane and biogenic CO₂, supporting farm income and strengthening agricultural resilience.

Figure 1 illustrates the proposed price floor mechanism. Large scale biogas production can provide downside protection to collapsing market prices by absorbing local market surpluses and turning them into biomethane and biogenic CO₂. Biomethane can easily be absorbed by the international natural gas market without affecting price. Similarly, the biogenic CO₂ may be absorbed by the to build CO₂ transport infrastructure, connecting Europe’s industrial centers to offshore storage sites. The remaining digestate will be returned to the farmers and reduce chemical fertilizer demand.

Europe has seen the consequences of unmanaged surplus before. Structural overproduction in cereals, sugar, and dairy has repeatedly triggered interventionist responses, from public stockpiles to export support. These measures have often been expensive, politically contested, and environmentally counterproductive. Without a more resilient outlet for surplus biomass, the system remains reactive.

Green molecules should therefore be treated as a strategic fallback market for agriculture. A network of large-scale anaerobic digestion (AD) co-digestion plants can provide an outlet for part of the excess production from multipurpose crops, residues, and manure, converting them into biomethane and biogenic CO₂. This can reduce the severity of price collapses by creating a credible alternative use for lower-value biomass.

To make this work in practice, farmers and project developers need flexible, large-scale digestion systems that can respond to changing harvest conditions. In strong harvest years, surplus biomass can be redirected into anaerobic digestion instead of being sold into distressed markets. In weaker years, preserved multipurpose crops can be prioritized for feed or other uses. This makes biomethane more than an energy product. It becomes a market mechanism that can reduce farmer distress, support more predictable revenues, and strengthen rural resilience.

What the economics suggest

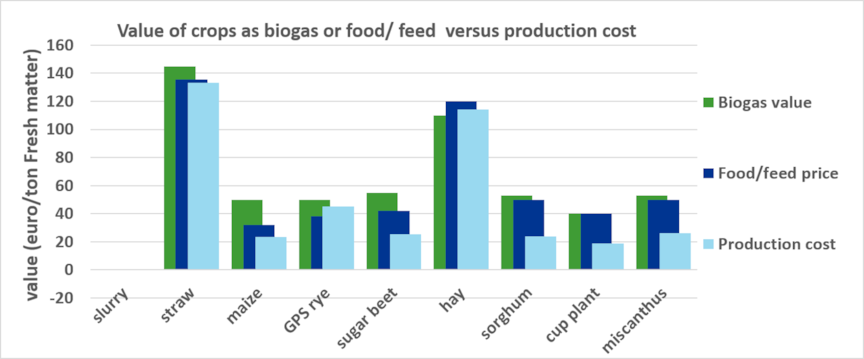

DNV’s assessment of a newly built large-scale biomethane plant (30 million m3), using a mix of manure, residues, and multipurpose crops, benchmarked crop values against maize silage. The figure below indicates that, in several cases, these price levels can compete with current food and feed market values and exceed variable production costs, excluding land-use costs. This supports the case for biomethane as a practical income floor for farmers.

Anaerobic digestion performs best when plants can run close to capacity on a relatively stable mix of manure and co-feeds. In practice, however, agriculture is exposed to weather extremes and fluctuating biomass availability, so digestion systems must be designed for variability.

Manure offers strong emissions benefits and can have low or even negative purchase costs, but its biogas yield per tonne is relatively low. Residues can improve output and often have a favourable emissions profile, but supply is limited and competing uses remain. Multipurpose crops can strengthen the digestion process, but they also introduce higher purchase costs and wider land-use-related emissions. Balancing these trade-offs requires cooperation between bio-energy parks, farmers, and knowledge institutes, supported by advanced modelling and optimization tools.

Policy implications

More than 80% of the EU’s annual EUR 57 billion in agricultural subsidies currently support the production of animals or animal feed, even though these products account for a large share of food-related greenhouse gas emissions[4]. If green molecules can provide an income floor for agriculture, then support for biomethane should not be viewed only as an energy subsidy, but also as part of agricultural market stabilization. Integrating biomethane demand into the EU Common Agricultural Policy, or into national frameworks such as the “Agreement on a Green Denmark”[5], would help align food security, farmer income stability, and energy resilience.

To conclude, green molecules should be understood not only as energy products, but as strategic tools for resilience. Recognizing biomethane in this way places it closer to the core of Europe’s future agricultural and energy system.

References:

- https://www.tridge.com/stories/dutch-onion-export-202223-historic-season-lower-volume-but-higher-value

- https://www.potatobusiness.com/market/european-potato-prices-collapse-to-eur15-per-tonne-amid-weak-demand/

- Source: Biogas cost model based on a newly build 30 MCM biomethane/yr facility in the Netherlands, as reviewed by DNV. Cost levels based on German data source (planungsdeckungsbeiträge 2024/2025 Nordrhein-westfalen). Note that the costs for sorghum , miscanthus, cup plant are indications only.

- https://www.universiteitleiden.nl/en/news/2024/04/how-eu-farm-subsidies-favour-high-emission-animal-products

- https://mgtp.dk/groent-danmark/english-a-greener-denmark/about-the-agreements-on-a-green-denmark