China's hydrogen play: scale today, energy security tomorrow

By Thomas Koller

China is undeterred by global headwinds facing hydrogen and its derivatives. In our new Hydrogen to 2060 forecast, we find around 35% of new hydrogen production and use globally will come from China over the coming decades. By 2060, 80% of all clean hydrogen produced in China, is renewable and produced by electrolysis. China’s scaling today is underpinned by industrial integration driving domestic demand.

Relentless scale and cost leadership

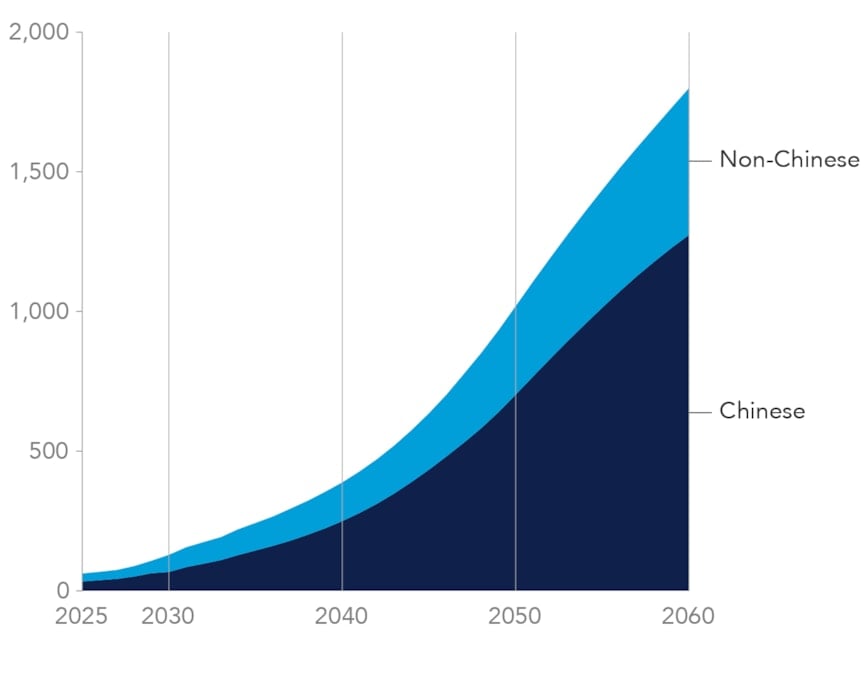

Dominance is built on clean technology manufacturing, rapid deployment and operational experience at scale. As we highlight in our forecast, China currently accounts for around 60% of global electrolyser deployment and investment decisions. Costs continue to decline due to sustained technology investment, local supply chains and access to low-cost capital. Production costs are roughly half those seen in many other markets, with projects scaling from tens to hundreds of megawatts within a few years.

Chinese electrolysers on track to dominate the market

Global cumulated electrolyser capacity additions (GW)

While international trade may still develop, near-term momentum favours projects that strengthen domestic energy independence, grid stability and industrial continuity in uncertain global energy market conditions.

Policy momentum accelerating market formation

Policy continues to reinforce this trajectory, with clean hydrogen scaling prominent in the 15th Five-Year Plan (2026 to 2030). Targets are linked to industrial decarbonization, energy security and technology leadership. China’s national Emissions Trading System is expanding in scope, with broader industrial coverage and aviation expected to be included by 2027, improving the economics for clean hydrogen. Provincial incentives, renewable integration mandates and hydrogen pilot clusters further support deployment. Unlike other economies where hydrogen development is dependent on subsidy, China’s policy mix is increasingly focused on enabling commercial viability, infrastructure build-out and demand stimulus across steel, chemicals, refining and emerging mobility segments.

DNV supporting safe scaling

Our work at DNV to support safe scaling of hydrogen sees us work with multi hundred-megawatt renewable hydrogen projects in China, building on our experience with demonstrators and small-scale projects globally. Our work spans feasibility, bankability assessments and compliance with emerging certification frameworks for the equipment, plant and clean molecules produced. Our verification and certification services can demonstrate compliance with Chinese regulations and support access to international markets through services such as European Union CE conformity assessment as a notified body.

Industrial decarbonization drives demand

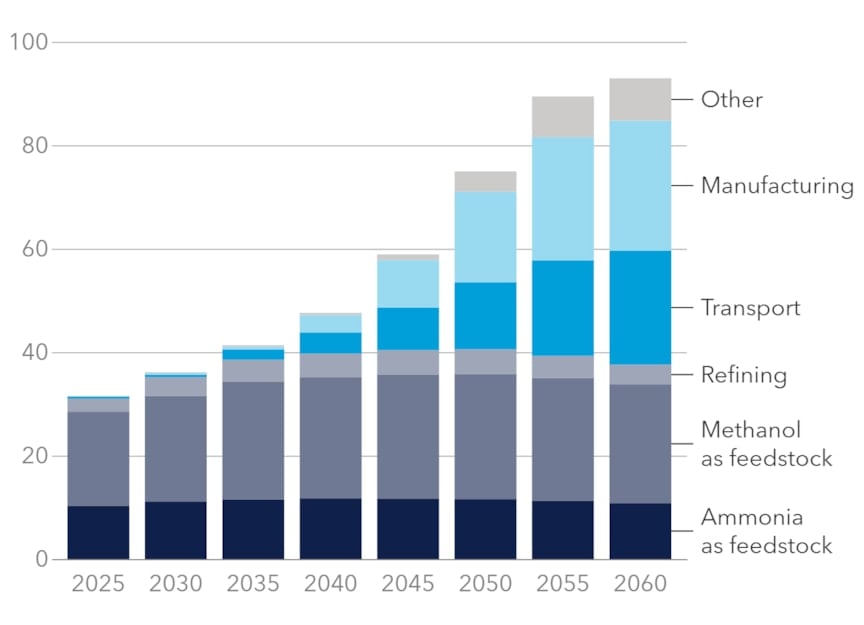

China has moved beyond early-stage demonstrators and the focus is on large-scale industrial decarbonization. Renewable hydrogen is being introduced into fossil dominant refineries. Other sources of demand include ammonia and methanol derivatives for use in transport as well as there being growing interest in steel via direct reduced iron pathways.

Greater China hydrogen demand by sector (MtH2/yr)

The emphasis is on integrating hydrogen into existing value chains where demand is substantial and infrastructure can be leveraged. At the same time, China continues to build domestic manufacturing leadership in electrolysers and components, which strengthens China’s export position even if the market for this is currently limited – China builds for the future. Export-oriented hydrogen remains secondary to domestic utilization in the near term. Cost reduction remains central, with optimization across the full value chain from renewable power to end-use.

Whole system integration to support energy security

In the next few years, China is expected to see rapid build-out of capacity as well as whole system optimization. We anticipate improved matching of variable renewables with electrolyser operation, expansion of hydrogen transport networks and the development of storage solutions.

As we see elsewhere in the world, recent volatility in the Middle East and wider geopolitical instability are sharpening China’s focus on energy security, and this reinforces the role of both clean and fossil hydrogen and derivatives for domestic deployment over export ambitions. China recognizes hydrogen as a strategic tool to reduce reliance on imported fossil fuels, particularly in hard-to-electrify industrial sectors. This is likely to accelerate investment in integrated PtX systems located close to demand centres. At the same time, supply chain resilience and technology self-sufficiency will remain priorities.