Negative electricity prices in France: a symptom of transition, not dysfunction

By Amaury Salauze

Negative electricity prices, once a rare curiosity in European markets, have rapidly become a defining feature of power systems with high renewable penetration. In France (as in most EU countries), their growing frequency is reshaping price dynamics and raising concerns among investors and asset owners. Far from signalling a structural flaw, these events reveal a system in transition, where regulation and incentives are still catching up with a rapidly evolving generation mix.

The new normal: when abundance drives prices below zero

The sharp increase in negative price events across Europe is, first and foremost, the result of a success: the massive deployment of renewable generation over the last couple of years (solar PV in particular), but also the return of nuclear production to pre-crisis levels.

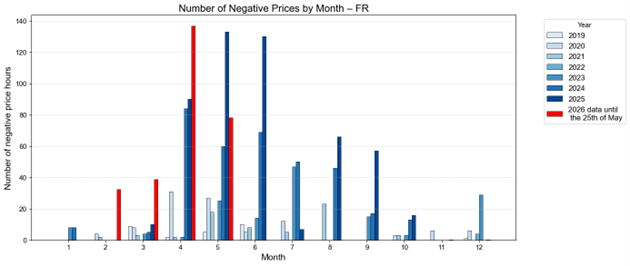

In France, this phenomenon is particularly visible during midday hours in spring and late summer, when solar output peaks while demand remains relatively moderate (see Figure 2). What used to be a handful of isolated hours has turned into recurring periods of oversupply, fundamentally impacting hourly price patterns.

In theory, negative prices are a perfectly rational outcome of an efficient market design. They reflect situations where some producers are willing to pay to keep producing rather than paying the higher costs associated with shutting down and restarting their power plants. This is especially relevant for conventional assets with technical constraints (nuclear, lignite, coal). However, the scale and persistence of negative prices observed today are a sign of something else.

Distorted signals: when market design meets legacy constraints

In practice, the recent surge in negative prices in France and the EU is not solely driven by physical system constraints, but also by the interaction between market signals and regulatory frameworks.

Two structural drivers stand out. First, the French nuclear fleet – while partially flexible – faces operational limitations that make deep or frequent modulation costly. Second, and more importantly, a significant share of renewable generation still operates under legacy support schemes (‘obligation d’achat’ contracts) that insulate producers from market prices. Under these mechanisms, generators have little to no incentive to reduce output when prices turn negative, leading to sustained oversupply.

The result is a system where negative prices no longer purely reflect optimal dispatch but also reveal misaligned incentives. This has important consequences for market participants: while some assets remain shielded from price signals, others – particularly merchant or partially exposed projects – face increasing revenue volatility and growing uncertainty around future returns.

Despite the increasing visibility of negative price events, most renewable projects in France remain relatively well protected from their direct financial impact. Assets operating under the historical feed-in tariff scheme (Obligation d’Achat, OA) are fully insulated from market price signals and therefore unaffected by negative prices. Similarly, projects under the Complementary Remuneration (CR) mechanism benefit from built-in safeguards such as the negative price premium (Pneg), which compensates for the non-payment of the CR premium in the case of negative prices.

A turning point: regulation, flexibility, and market rebalancing

Recognizing these distortions, targeted reforms have recently been introduced to restore efficient price signals. Adjustments to support schemes are progressively incentivizing renewable producers to curtail output during periods of negative prices, while new provisions allow for the active modulation of capacity that was previously insensitive to price signals.

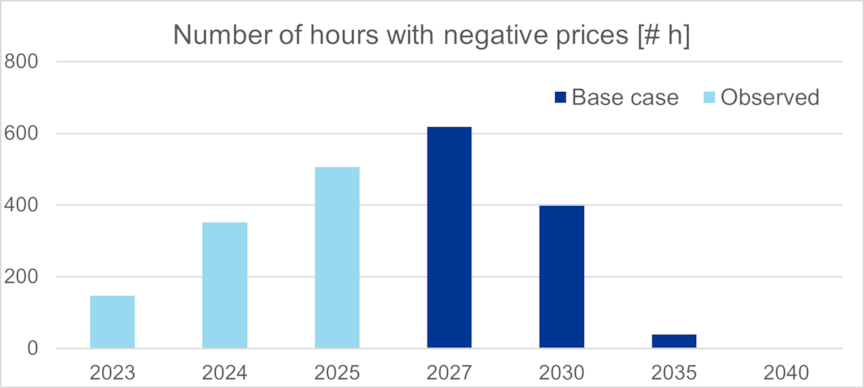

These changes are already shifting market behaviour. In the short term, they are expected to reduce the depth of negative prices, even if their frequency remains significant due to continued renewable expansion. Over the longer term, structural trends point to a gradual rebalancing with diminishing pressure.

The phase-out of legacy contracts, combined with the deployment of more flexible renewable assets, will increase responsiveness to price signals. At the same time, the development of flexibility solutions – such as battery storage, demand-side response, and electrification – will help absorb excess generation. Across Europe, the progressive retirement of inflexible thermal assets (lignite, coal) will further contribute to a more adaptable system.

One key uncertainty remains: the future role of nuclear flexibility in France. Its operational strategy can significantly influence the pace and extent of market adjustment.

From DNV’s perspective, understanding negative price dynamics requires a granular and forward-looking approach. Leveraging its Power Price Forecasts model and local regulatory expertise, DNV can estimate the future frequency of negative price events with a high level of confidence and under different scenarios.

Through detailed hourly modelling of the market, DNV can accurately assess the real impact of negative prices across different assets and contracts. This enables DNV to support its clients in quantifying exposure, identifying when negative prices constitute a downside risk, and, conversely, when they may create opportunities.

Conclusion: from volatility to visibility

Negative electricity prices are often perceived as a warning signal for investors. In reality, they are more of a transitional feature of an energy system undergoing rapid transformation. They do not necessarily indicate a flawed power mix, but rather a temporary mismatch between market rules, legacy support schemes, and the evolving fundamentals of supply and demand.

Beyond negative prices, it becomes increasingly challenging for market participants to navigate a market with more frequent periods of very low prices, anticipate their trajectory, and integrate them into decision-making. Asset valuation, contract structuring, hedging, and investment strategies increasingly depend on a precise understanding of hourly price dynamics.

In a power system where intraday volatility is growing, average prices are no longer sufficient to assess asset profitability: capture prices and revenues depend critically on the timing of production and the occurrence of extreme price events.

This is precisely the value provided by DNV. Through its Power Analytics platform, DNV delivers the results of its power price forecasts, combining a robust fundamental modelling approach with advanced machine learning techniques. This multi-layer methodology allows for a detailed representation of future power system trends while maintaining a high level of granularity in hourly price variations.

As a result, clients benefit from reliable estimates of captured prices and asset profitability, enabling more informed decisions in an increasingly complex and volatile market environment.